Caltos: Scaling enterprise lending without increasing operational risk

Loan Management System

SaaS

Fintech

Role: Lead Product Designer · 2025

Scaling enterprise lending through operational clarity

View live product

TL;DR

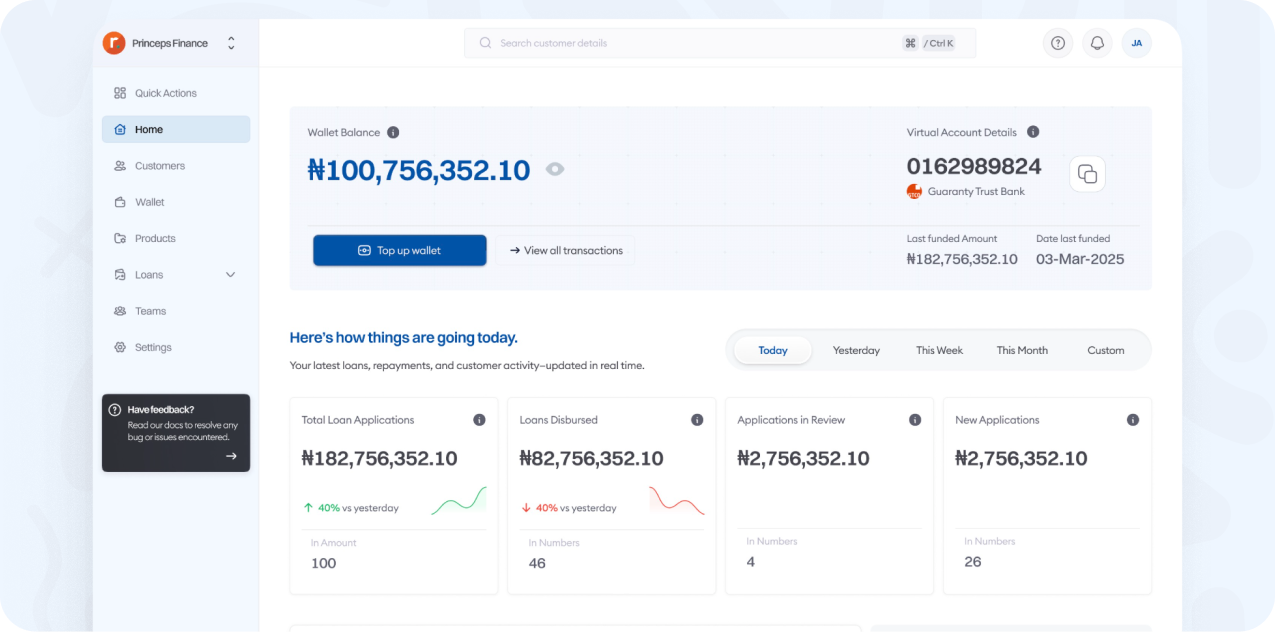

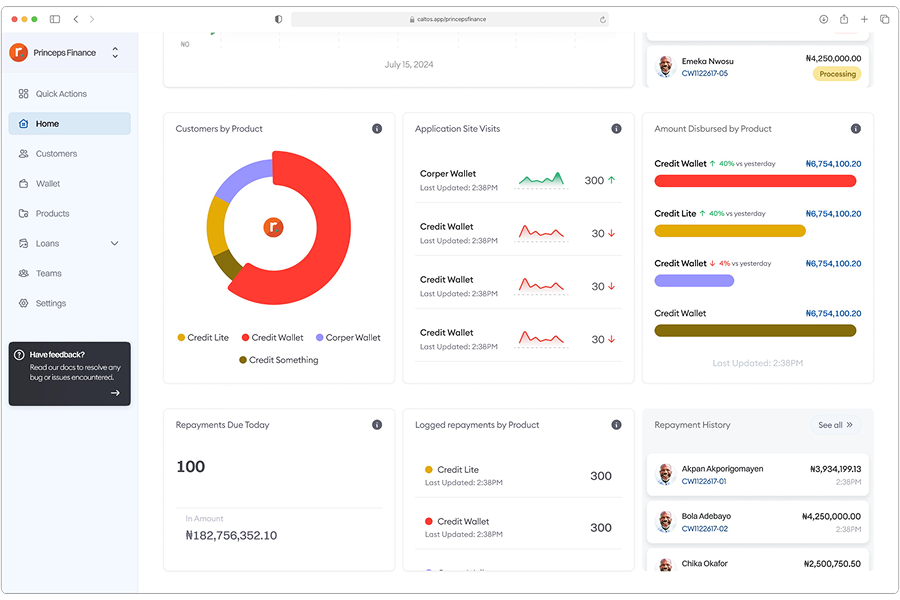

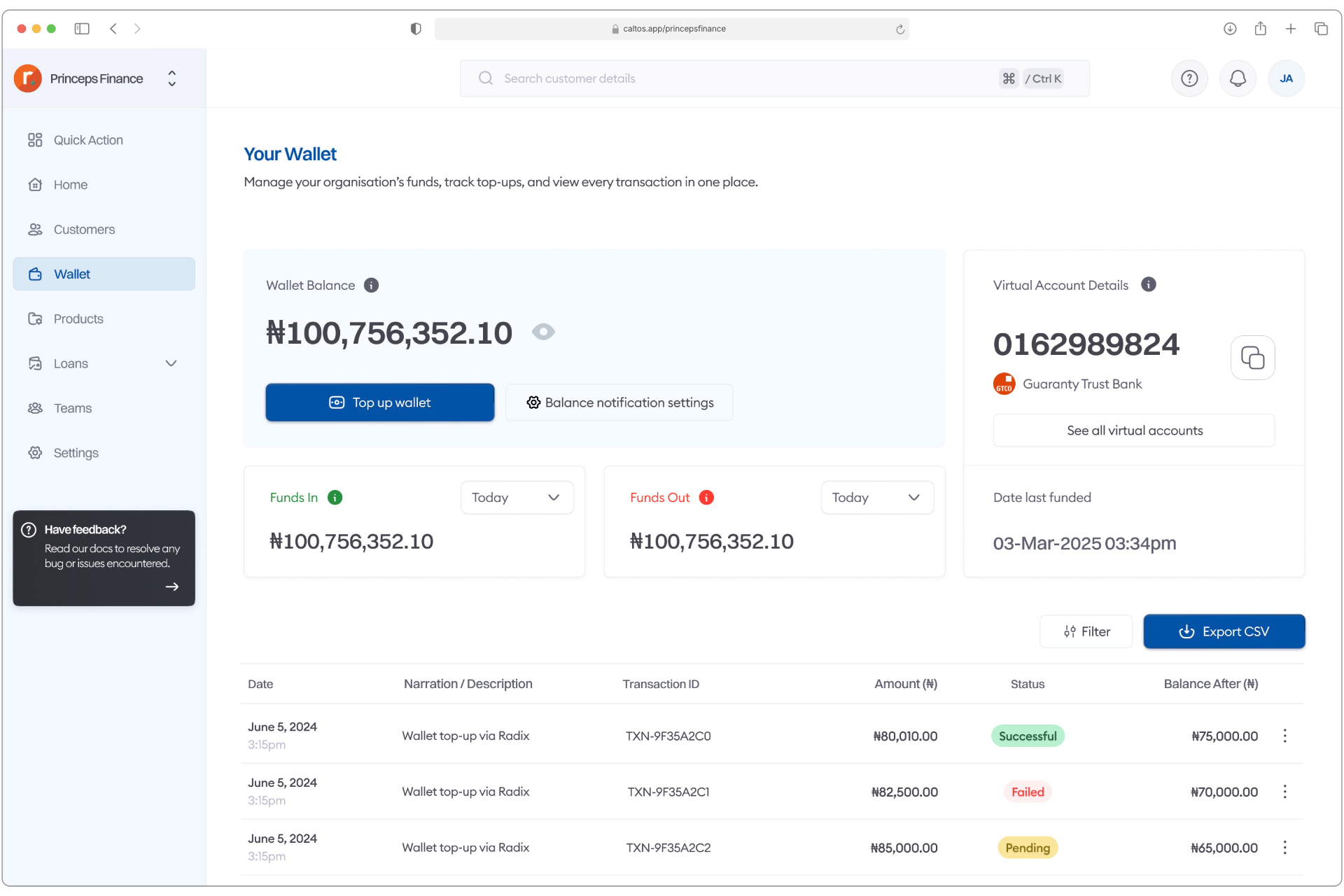

- ₦7.3B+ processed across multiple live lending companies

- Designed an end-to-end loan operations platform for lending businesses

- Enabled non-technical teams to launch and manage loan products without engineering dependency

- Improved collection efficiency by 70%

Context

Lending businesses often rely on fragmented tools, rigid vendor platforms, or heavy engineering involvement to launch loan products. This slows time-to-market and introduces operational risk.

Caltos was designed to centralise loan creation, management, and recovery into a single system that could scale safely across different lending models.

Core Design Challenge

How do you give lending teams flexibility to create diverse loan products without overwhelming them with complexity or introducing operational errors?

Key Design Decisions

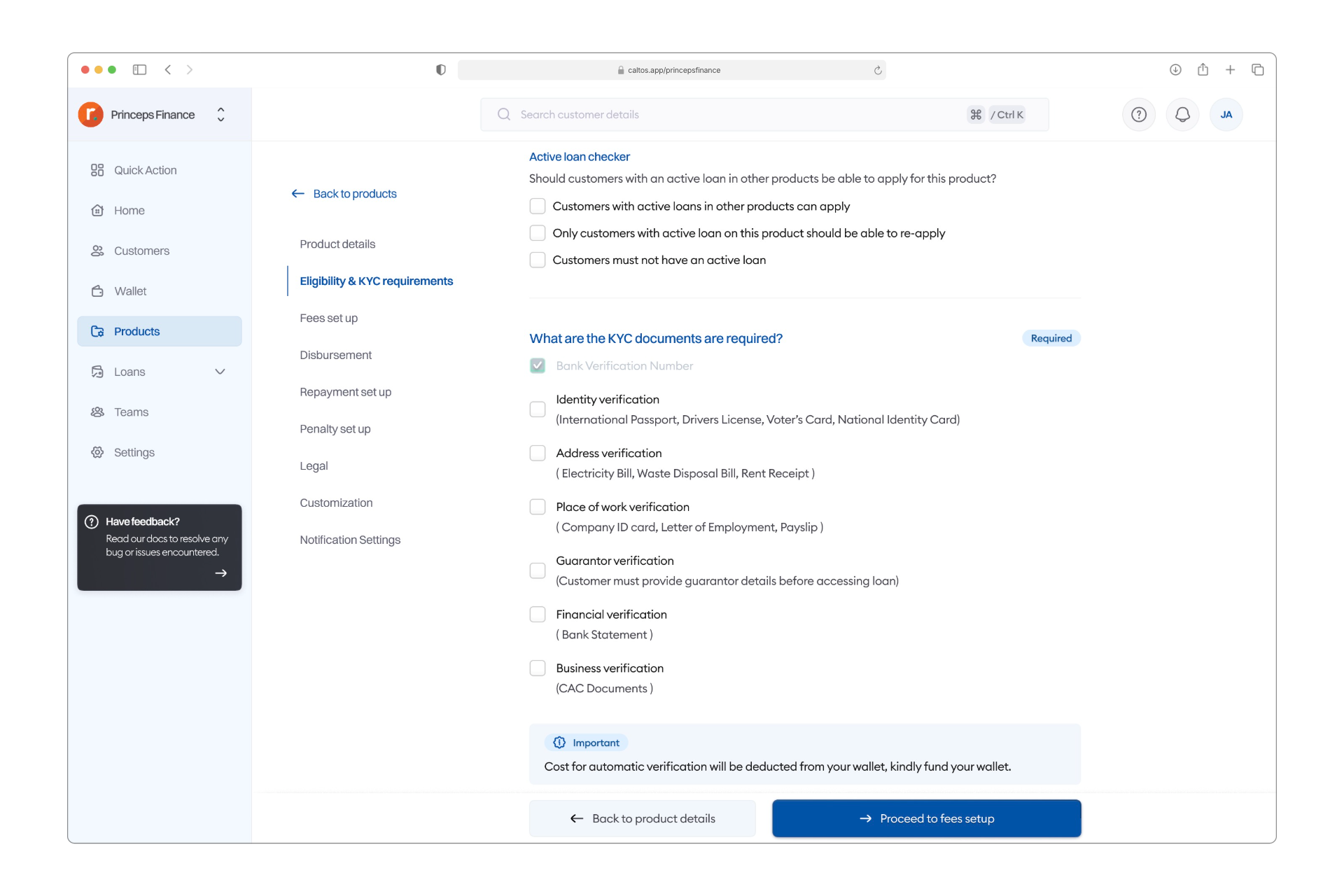

- Eligibility-first loan creation to set expectations early and reduce dead-end applications

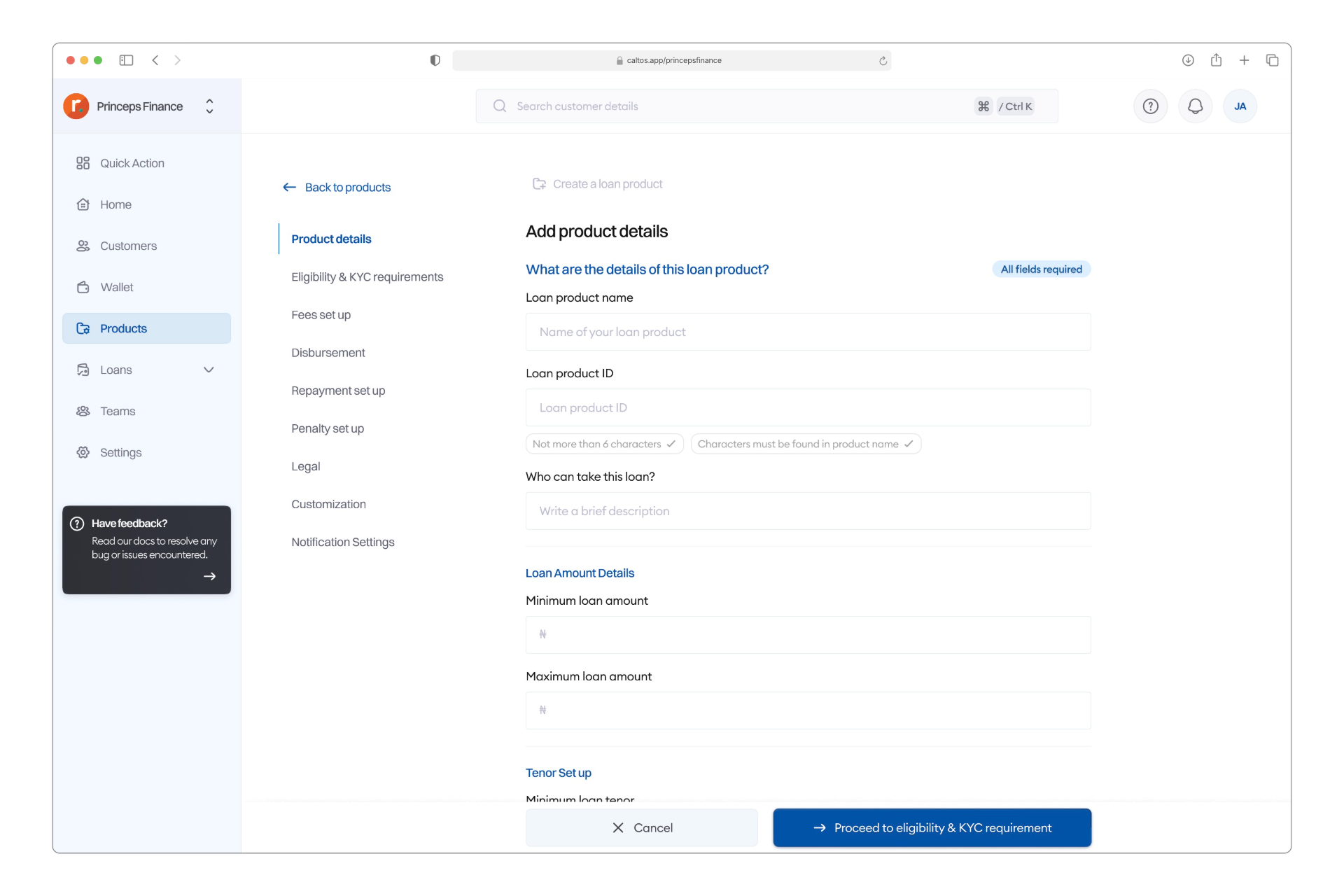

- Step-based product setup to guide non-technical operators through complex configurations

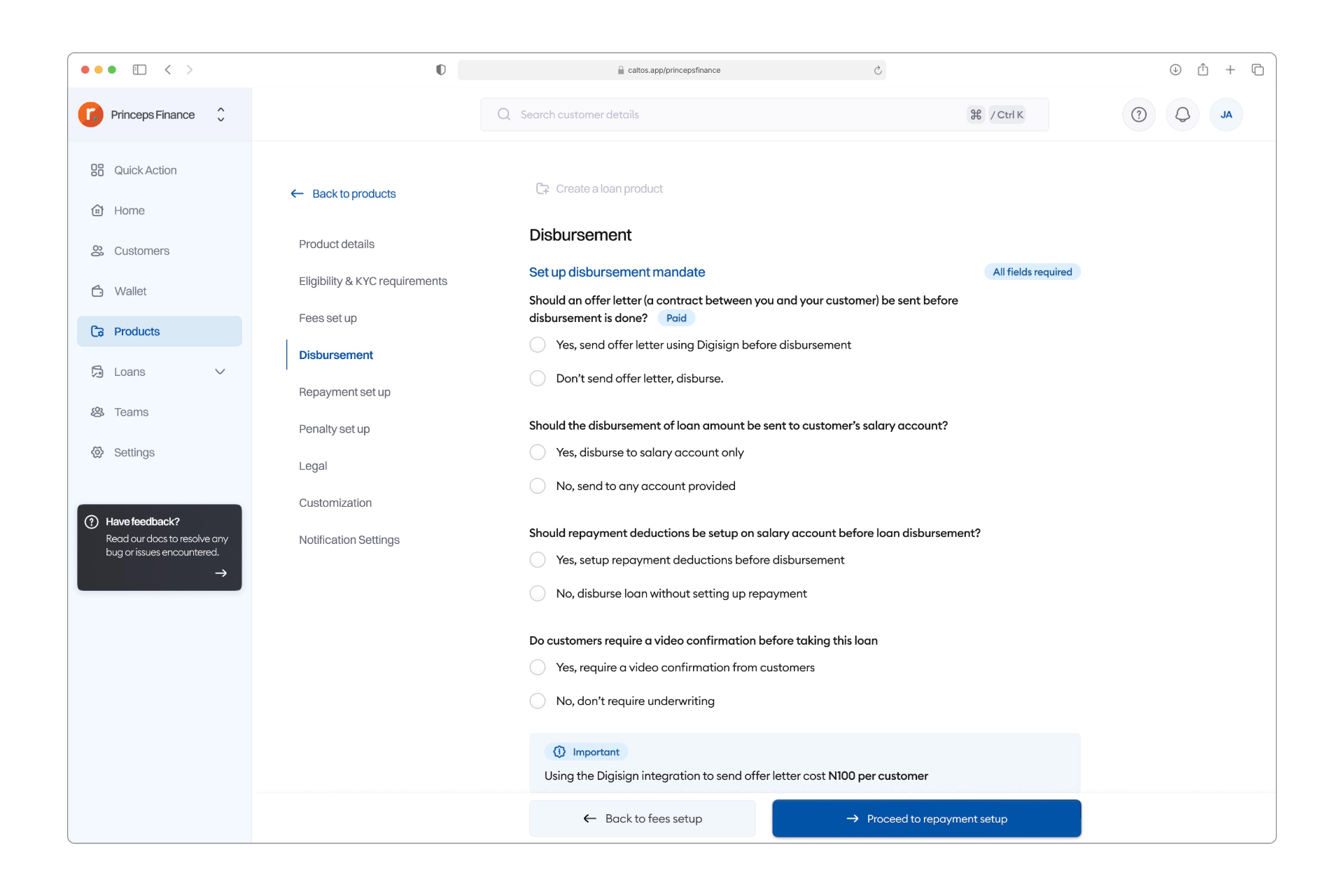

- Repayment and recovery as first-class flows, embedded directly into product setup

- Fraud and risk guardrails to prevent payout, mandate, and recovery failures

Outcome

- ₦7.3B+ processed across loan products

- Loan product time-to-market reduced by months

- Multiple lending companies operating on the platform

- Reduced engineering dependency for lending operation

Insights That Shaped the Product

- Loan products were constrained by rigid, predefined buckets.

- Eligibility was surfaced only at rejection, leaving users without context or alternatives.

Rigid structures slow experimentation. Rejection-first eligibility breaks trust and kills recoverable demand. Both patterns needed to be redesigned.

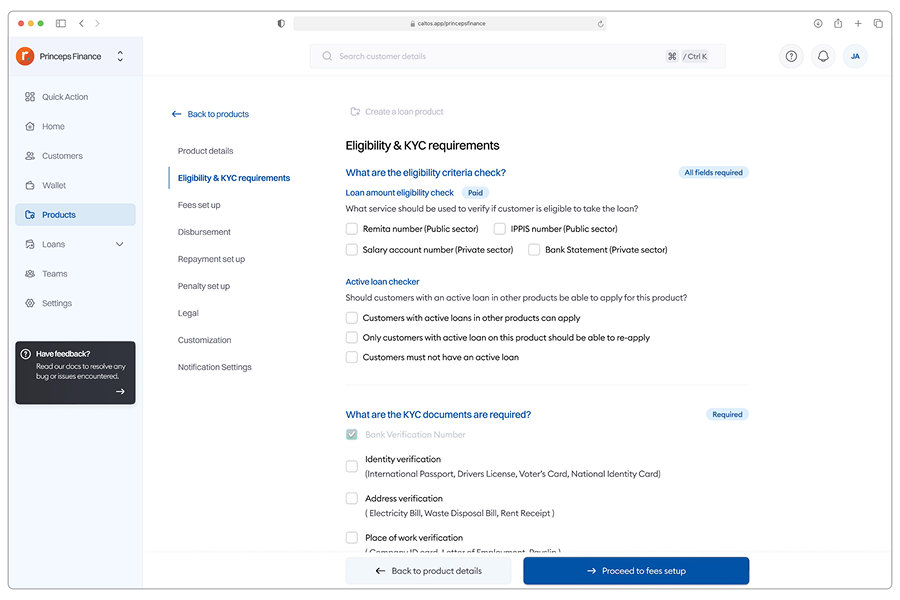

Loan Product Creation for Non-Technical Teams

A single dense configuration screen would have made errors inevitable.

A guided setup was necessary for non-technical teams configuring live loan products.

Loan creation was designed as a step-by-step flow that breaks complex configuration into clear, sequential decisions. This reduced setup errors, lowered cognitive load, and allowed teams to ship loan products without engineering support

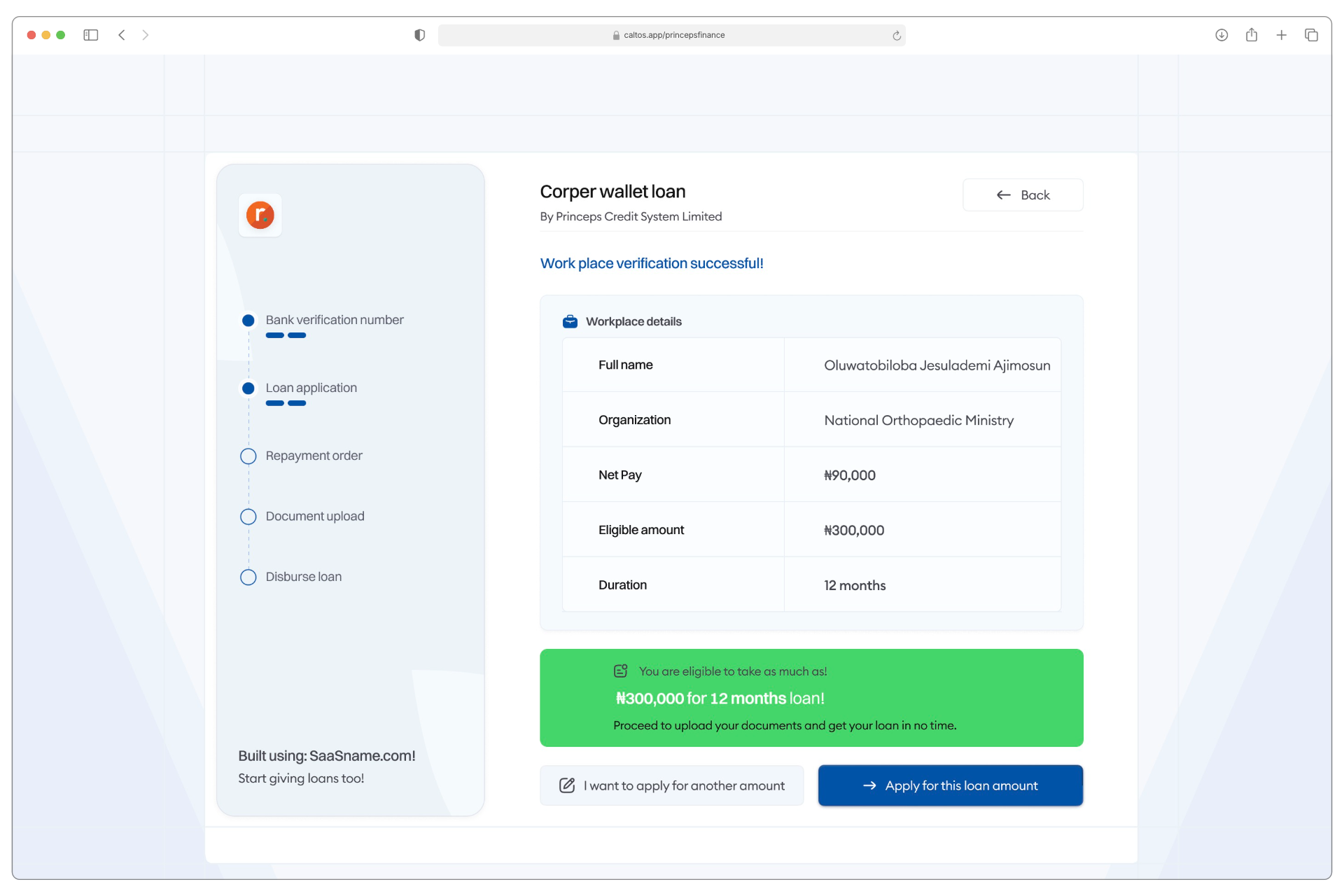

Eligibility as a Flexible System

Surfacing eligibility only at rejection breaks trust. Eligibility needed to be understood before commitment, not after failure.

Caltos treats eligibility as a flexible system rather than a fixed rule set, supporting different lending models (civil service, private sector, government workers). This allows users to understand their standing early and enables businesses to responsibly offer alternatives when appropriate.

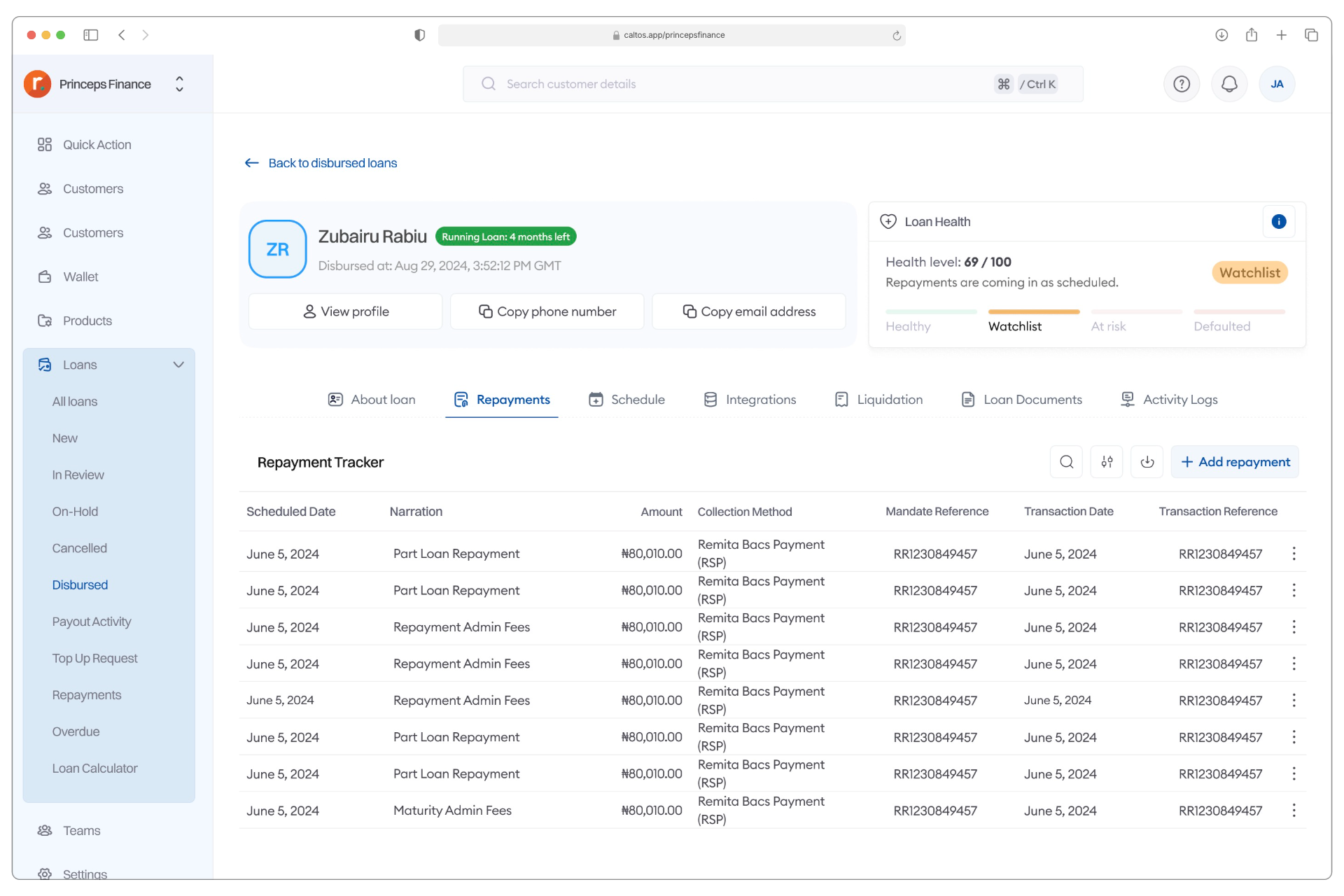

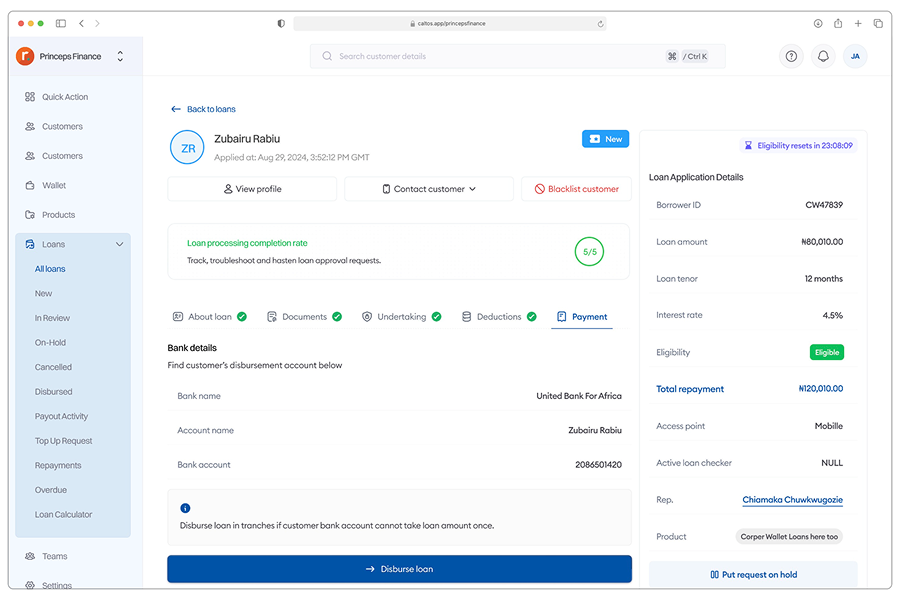

Designing for Repayment and Reconciliation

Loans do not end at disbursement. Any system that treats repayment as an afterthought creates operational debt.

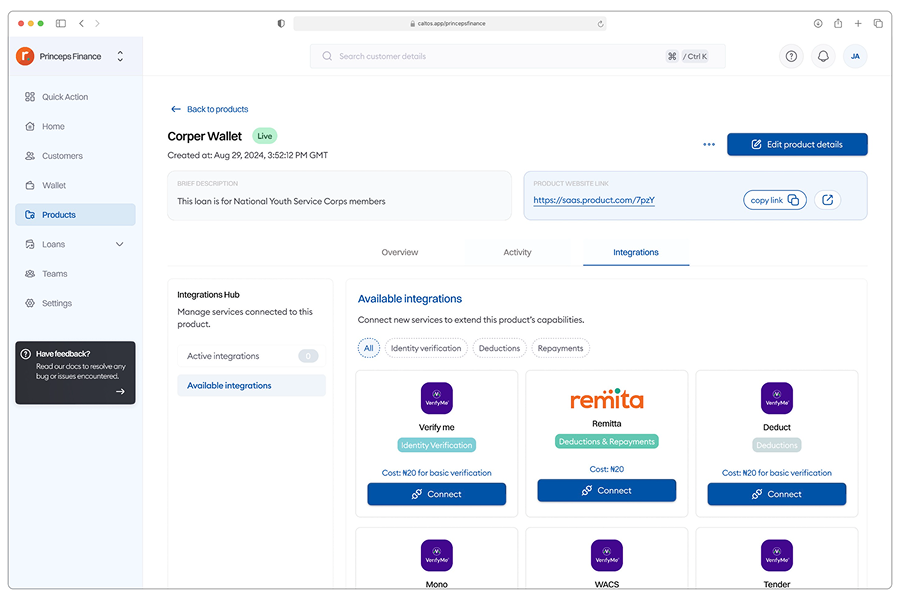

Repayment structure and frequency are defined during product setup, preventing downstream bottlenecks. Integration with direct debit services improves collections and simplifies reconciliation across loan products.

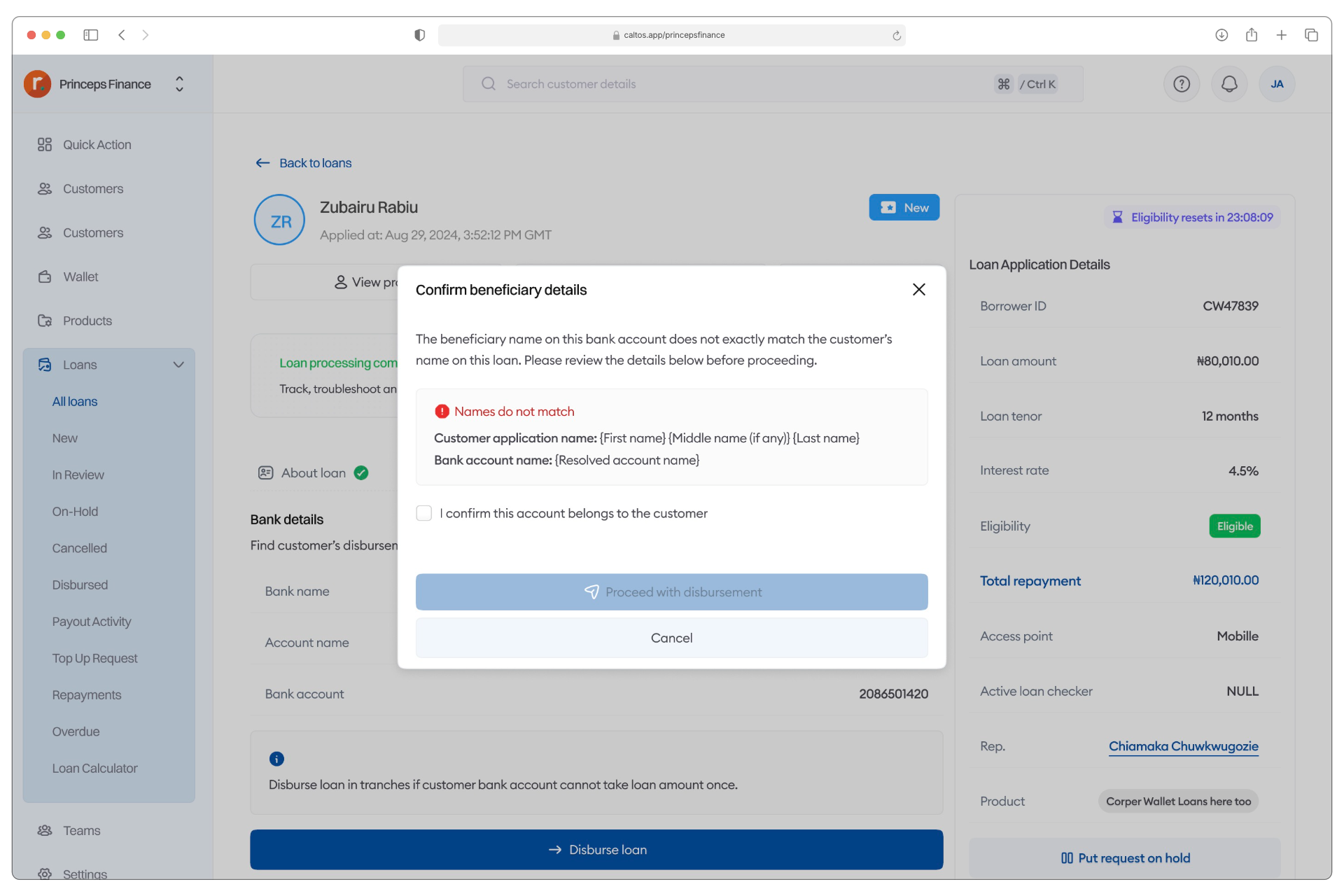

Fraud Risk and Guardrails

In lending systems, small shortcuts lead to large losses.

Caltos embeds guardrails directly into the flow:

- identity verification

- salary-account-aligned payouts

- repayment mandates before disbursement

- historical loan checks where applicable

These controls reduce risk while keeping operations predictable.

What Drove Adoption

Adoption was driven by:

- plain language instead of loan jargon

- guided decisions instead of dense forms

- clarity over compressed, one-screen workflows

The system remained powerful without becoming fragile.

Learnings

The first version of Caltos was too narrowly scoped. That constraint limited adoption.

Expanding the system to support broader lending models became the most important shift in the product’s growth. Designing for real-world behaviour — including misuse and misunderstanding — proved more critical than designing for ideal users.

What This Project Demonstrated

- Designing fintech systems beyond UI

- Translating financial rules into usable workflows

- Handling repayment, eligibility, and failure states

- Designing for real operational constraints